"I suppose it is tempting, if the only tool you have is a hammer, to treat everything as if it were a nail." - Albert Maslow

"If you don't have a hammer, you will treat everything as a hammer." - Me

Tuesday, July 16, 2013

Sunday, July 14, 2013

Contrasting Stories

This morning I was thinking about what the future of the US securities market was going to look like. I assume it will move to further automation. But how will regulation attempt to keep up with it? Then I saw this story

ThisDayLive: Ajomale: It is Absolutely Necessary for Nigeria to Have an OTC Market

My first thought was "Oh no. Should I expect to soon start receiving a flurry of emails from wealthy West African broker dealers offering to share with me their family's vast wealth of credit default swaps if only I will agree to novate those positions to my clearing account?"

On a more serious note - the story is an interview with the the CEO of the Nigerian Association of Securities Dealers (also known as NASD) about how Nigerian securities brokers are trying to set up an OTC market. From that story

"Most of the time people see a market as only a trading platform, but behind the trading platform are rules, in front of the rules are operators, behind all the transactions there must be a bank and for a transaction to run smoothly there must be a clearing house. So all these peripherals we have put them in place in addition to getting a platform."

So they are forced to think about all of the same issues that we face in the US and will continue to face as our securities market increases in its complexity. However contrast that story with this one in the same newspaper

ThisDayLive: Shekau Denies Boko Haram Ceasefire

This second story is about Boko Haram the militant Islamist movement that operates in the Northern Nigerian state of Yobe. The name Boko Haram means "Western education is sinful" or "Western education is forbidden". The group's primary activity seems to be blowing up schools and Christian churches. They could be considered to be the Taliban's West African cousin. Last week they massacred 29 school children. In a world filled with vile militant groups this is truly one of the most vile. In case you were wondering Nigeria has a population of approximately 170 MM people and a 61% literacy rate. Meaning they have approximately 66 MM illiterate persons.

But soon they may have an OTC securities market. I can't wait to start receiving those emails.

ThisDayLive: Ajomale: It is Absolutely Necessary for Nigeria to Have an OTC Market

My first thought was "Oh no. Should I expect to soon start receiving a flurry of emails from wealthy West African broker dealers offering to share with me their family's vast wealth of credit default swaps if only I will agree to novate those positions to my clearing account?"

On a more serious note - the story is an interview with the the CEO of the Nigerian Association of Securities Dealers (also known as NASD) about how Nigerian securities brokers are trying to set up an OTC market. From that story

"Most of the time people see a market as only a trading platform, but behind the trading platform are rules, in front of the rules are operators, behind all the transactions there must be a bank and for a transaction to run smoothly there must be a clearing house. So all these peripherals we have put them in place in addition to getting a platform."

So they are forced to think about all of the same issues that we face in the US and will continue to face as our securities market increases in its complexity. However contrast that story with this one in the same newspaper

ThisDayLive: Shekau Denies Boko Haram Ceasefire

This second story is about Boko Haram the militant Islamist movement that operates in the Northern Nigerian state of Yobe. The name Boko Haram means "Western education is sinful" or "Western education is forbidden". The group's primary activity seems to be blowing up schools and Christian churches. They could be considered to be the Taliban's West African cousin. Last week they massacred 29 school children. In a world filled with vile militant groups this is truly one of the most vile. In case you were wondering Nigeria has a population of approximately 170 MM people and a 61% literacy rate. Meaning they have approximately 66 MM illiterate persons.

But soon they may have an OTC securities market. I can't wait to start receiving those emails.

Saturday, July 13, 2013

Income of USD 200,000 doesn't make you rich (or smart)

Note to SEC: 200,000 Doesn't Mean You're Rich - James Grieff

"The Securities and Exchange Commission today approved an end to a long-standing rule that barred hedge funds and private investment groups from advertising to seek capital from the public...The 80-year-old ad ban placed limits on how certain funds could solicit money from the general public for "private placements" -- investment arrangements that are exempt from SEC registration rules and their accompanying financial disclosures...Although the SEC had to end the ban, it didn't have to leave intact outdated standards outlining which investors would be allowed to put money into private placements. For individuals, such "accredited investors" are still defined as those with annual incomes of USD 200,000 ( USD 300,000 for a couple) and a net worth of USD 1 million. To its credit, the agency two years ago decided to exclude a primary residence from the net worth calculation...Those thresholds were set in 1982, when USD 200,000 was worth a lot more than it is today. Thanks to inflation, you would need to make almost USD 500,000 a year to have the same standard of living."

A few years back I took the Series 24 exam to be a securities principle ie a person who supervises stock brokers and broker dealer firms. As I was reading through the virtual telephone book of rules I wondered which rules had been violated that led to the 2007-2008 meltdown. The only ones that I could find were possibly disclosure rules - in that some MBS/CMO salesmen may have known that they were selling securities that had a significant probability of going into default and yet they did not reveal this to the customer. However considering the banks held on to a lot of these same securities themselves I question how much the CMO salesmen really knew.

That is a bit of a sad commentary - all these securities rules (and there are a ton) and they don't protect us from a major financial meltdown. How much good are the rules really doing? What it appeared to me was that the focus of the rules were to protect the individual retail investor from unscrupulous con men. But that was not what nearly took down the system. On the other hand if not for the existence of that telephone book sized set of rules to cover the behavior of securities salesmen perhaps unscrupulous con men would be a huge problem. We don't see a huge problem now because the rules are in place. And this is the point that I want to make - the change referenced in the Grieff article loosens the reigns a bit. We should be very careful when doing this. Maybe advertising should be allowed but the rules were there for a purpose. And Grieff is right to suggest that now might be a good time to update the income requirements.

"The Securities and Exchange Commission today approved an end to a long-standing rule that barred hedge funds and private investment groups from advertising to seek capital from the public...The 80-year-old ad ban placed limits on how certain funds could solicit money from the general public for "private placements" -- investment arrangements that are exempt from SEC registration rules and their accompanying financial disclosures...Although the SEC had to end the ban, it didn't have to leave intact outdated standards outlining which investors would be allowed to put money into private placements. For individuals, such "accredited investors" are still defined as those with annual incomes of USD 200,000 ( USD 300,000 for a couple) and a net worth of USD 1 million. To its credit, the agency two years ago decided to exclude a primary residence from the net worth calculation...Those thresholds were set in 1982, when USD 200,000 was worth a lot more than it is today. Thanks to inflation, you would need to make almost USD 500,000 a year to have the same standard of living."

A few years back I took the Series 24 exam to be a securities principle ie a person who supervises stock brokers and broker dealer firms. As I was reading through the virtual telephone book of rules I wondered which rules had been violated that led to the 2007-2008 meltdown. The only ones that I could find were possibly disclosure rules - in that some MBS/CMO salesmen may have known that they were selling securities that had a significant probability of going into default and yet they did not reveal this to the customer. However considering the banks held on to a lot of these same securities themselves I question how much the CMO salesmen really knew.

That is a bit of a sad commentary - all these securities rules (and there are a ton) and they don't protect us from a major financial meltdown. How much good are the rules really doing? What it appeared to me was that the focus of the rules were to protect the individual retail investor from unscrupulous con men. But that was not what nearly took down the system. On the other hand if not for the existence of that telephone book sized set of rules to cover the behavior of securities salesmen perhaps unscrupulous con men would be a huge problem. We don't see a huge problem now because the rules are in place. And this is the point that I want to make - the change referenced in the Grieff article loosens the reigns a bit. We should be very careful when doing this. Maybe advertising should be allowed but the rules were there for a purpose. And Grieff is right to suggest that now might be a good time to update the income requirements.

MF autopsy

Scott Skyrm's new book the The Money Noose is a fascinating read (at least for those who enjoy finance related topics) detailing the events which led up to the 2011 demise of broker MF Global.

A brief review of the story: in 2010 Jon Corzine was named the CEO of broker MF Global. At the time MF was struggling due to high costs and low interest rates and was in danger of being downgraded by the ratings agencies. Corzine was uniquely positioned for this role as he had previously served as the managing partner at Goldman Sachs (prior to being elected as Senator and later Governor of NJ). His plan was to transform the mid sized broker-centric MF into a full service investment bank modeled on Goldman. However he was in a race to avoid the ratings agencies downgrading MF to non-investment grade. An event which would preclude MF from becoming a first tier financial firm.

In an effort to boost MF's revenues until his proposed changes could be effected Corzine and a small trading team effected larger and larger trades using MFs money. The trades that they engaged in consisted of buying distressed European debt (from Portugal, Italy, Ireland, and Spain - four of the PIIGS) with the understanding that the EU had effectively insured this debt. Corzine's team purchased substantially more distressed debt than MF had funds to pay for. They did this by borrowing money from other brokers and then collateralizing the loans using the debt that they had just purchased. It is actually a bit more complicated than this - but that is the idea. While in theory the debt that MF purchased was insured against default - MF nevertheless fell prey to it.

In 2011 the markets became nervous about the PIIGS possibly defaulting and the prices of the bonds that MF had purchased fell (even if they were effectively insured). MF was forced to post more and more of their own funds as additional collateral to guarantee the broker loans. Eventually these collateral requirements strained MFs ability to raise cash. With MF struggling both with revenues and overextended on this trade they became victim to what amounts to a bank run - as their counterparties began reduce lending lines to MF and increased collateral requirements on them. When the ratings agencies finally downgraded them the wheels came off and MF was in a life struggle to raise cash to keep going.

In the last days of MF as they fought to keep themselves afloat funds were taken from customer accounts and used to cover MFs obligations. Whether this was done intentionally or not and who was involved in authorizing and moving the funds is still an open question. When MF finally declared bankruptcy it was discovered that their customer accounts were missing approximately USD 891 MM.

Skyrm is well suited to tell this story as in his previous employment at Newedge he headed a fixed income / repo desk - so he knows the market well. Overall I found the book fascinating with the most interesting portion being the few weeks before the blow up - seeing what was effectively a slow motion bank run. If you liked When Genius Failed (about Long Term Capital Management) then you will like this story as well. Interestingly Corzine shows up in both books.

My one criticism is this. In telling the story Skyrm was faced with a bit of a dilemma. The exact mechanics of the trades in question and some of the accounting issues which would eventually bite MF are a bit complex. Should he explain the mechanics in detail so the reader has a full understanding - but at the risk of losing some readers? Or should he try to simplify the story somewhat for the lay reader? I would have preferred that he leaned a little harder in the first direction. I think he simplified a bit too much. But that is a small criticism. I recommend this book.

* In the interests of transparency I previously worked with Skyrm and a few of the characters in the book at Fimat / Newedge. I don't know him that well but we did have some interactions.

A brief review of the story: in 2010 Jon Corzine was named the CEO of broker MF Global. At the time MF was struggling due to high costs and low interest rates and was in danger of being downgraded by the ratings agencies. Corzine was uniquely positioned for this role as he had previously served as the managing partner at Goldman Sachs (prior to being elected as Senator and later Governor of NJ). His plan was to transform the mid sized broker-centric MF into a full service investment bank modeled on Goldman. However he was in a race to avoid the ratings agencies downgrading MF to non-investment grade. An event which would preclude MF from becoming a first tier financial firm.

In an effort to boost MF's revenues until his proposed changes could be effected Corzine and a small trading team effected larger and larger trades using MFs money. The trades that they engaged in consisted of buying distressed European debt (from Portugal, Italy, Ireland, and Spain - four of the PIIGS) with the understanding that the EU had effectively insured this debt. Corzine's team purchased substantially more distressed debt than MF had funds to pay for. They did this by borrowing money from other brokers and then collateralizing the loans using the debt that they had just purchased. It is actually a bit more complicated than this - but that is the idea. While in theory the debt that MF purchased was insured against default - MF nevertheless fell prey to it.

In 2011 the markets became nervous about the PIIGS possibly defaulting and the prices of the bonds that MF had purchased fell (even if they were effectively insured). MF was forced to post more and more of their own funds as additional collateral to guarantee the broker loans. Eventually these collateral requirements strained MFs ability to raise cash. With MF struggling both with revenues and overextended on this trade they became victim to what amounts to a bank run - as their counterparties began reduce lending lines to MF and increased collateral requirements on them. When the ratings agencies finally downgraded them the wheels came off and MF was in a life struggle to raise cash to keep going.

In the last days of MF as they fought to keep themselves afloat funds were taken from customer accounts and used to cover MFs obligations. Whether this was done intentionally or not and who was involved in authorizing and moving the funds is still an open question. When MF finally declared bankruptcy it was discovered that their customer accounts were missing approximately USD 891 MM.

Skyrm is well suited to tell this story as in his previous employment at Newedge he headed a fixed income / repo desk - so he knows the market well. Overall I found the book fascinating with the most interesting portion being the few weeks before the blow up - seeing what was effectively a slow motion bank run. If you liked When Genius Failed (about Long Term Capital Management) then you will like this story as well. Interestingly Corzine shows up in both books.

My one criticism is this. In telling the story Skyrm was faced with a bit of a dilemma. The exact mechanics of the trades in question and some of the accounting issues which would eventually bite MF are a bit complex. Should he explain the mechanics in detail so the reader has a full understanding - but at the risk of losing some readers? Or should he try to simplify the story somewhat for the lay reader? I would have preferred that he leaned a little harder in the first direction. I think he simplified a bit too much. But that is a small criticism. I recommend this book.

* In the interests of transparency I previously worked with Skyrm and a few of the characters in the book at Fimat / Newedge. I don't know him that well but we did have some interactions.

Monday, July 08, 2013

Rick Perry's big announcement

And I will tell you its three positions in government that Rick Perry will not be running for. President, Governor, and the um ...um whats the third one there? Lets see. President...um five? ok so President, Governor, and um the uh uh...EPA?...no sir no sir we were talking about the three positions in government that he will not be running for are President, Governor, and lets see uh ...I can't...umm...I can't think of...oops.

It never gets old.

It never gets old.

Sunday, July 07, 2013

Thank you Glenn Beck

"Dear Glenn:

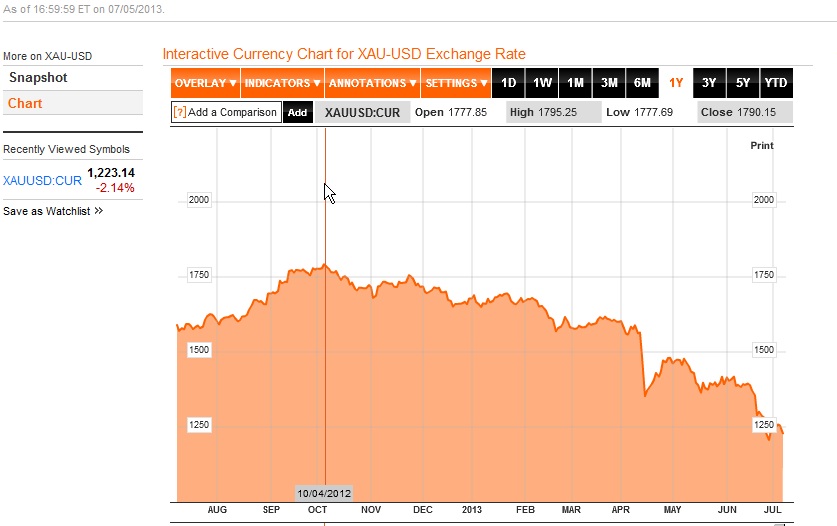

Back in September I finally made the move. After reading your column (here) discussing the Fed's extension of QE3 I was convinced. Hyperinflation was on the imminent horizon. So heeding your warning I took all of my money out of banks (like you suggested), sold my stocks and bonds, and bought gold. Fortunately your associates at Goldline were so willing to help me convert my life savings of USD 300,000 into gold coins. Unfortunately that has not worked out so well. At the time I bought gold it was selling for USD 1760 / toz. Now - just 9 months later - gold is selling for USD 1223 / toz - down 32%. Due to this move I have lost nearly USD 100,000 or 1/3 of my life savings - in just 9 months. I am sincerely puzzled how this could happen considering that gold is the "safe haven" asset. I can only surmise that the globalist bankers, the radical socialists, and their allies in the Muslim Brotherhood are conspiring to discredit you and your associates at Goldline. On the positive side I have avoided the massive hyperinflation that we have experienced over the last year. Since I invested in gold the CPI has risen from 231.6 to 231.8 a 1/10th of 1% increase. Thank you so much for your help.

Your friend - ROB"

Ok in case you were wondering - I am not a moron. I did not really put my life savings into gold. But considering Glenn has nearly 1MM monthly listeners getting a constant dose of paranoia and gold-bug drivel I will bet that someone did exactly what I suggested in the above letter. Again I am not a moron, I did not invest in gold, and there is no hyperinflation. For more on this last point see Paul Krugman's response to Eric Erickson on the price of milk and bread (see here).

Actually to put this into perspective the writer of the fictitious letter above lost 1/3 of his savings over the last 9 months by investing in gold. How far back would we have to go in order for the loss due to inflation to be equal to a loss of 1/3 of savings? If you go back to June of 1996 the CPI was at 152. Today the CPI is at 231. Meaning that over the last 17 years a dollar has lost 1/3 of its purchasing power due to inflation (152/231 = .66). That is assuming you earned 0 interest on your savings.

Back in September I finally made the move. After reading your column (here) discussing the Fed's extension of QE3 I was convinced. Hyperinflation was on the imminent horizon. So heeding your warning I took all of my money out of banks (like you suggested), sold my stocks and bonds, and bought gold. Fortunately your associates at Goldline were so willing to help me convert my life savings of USD 300,000 into gold coins. Unfortunately that has not worked out so well. At the time I bought gold it was selling for USD 1760 / toz. Now - just 9 months later - gold is selling for USD 1223 / toz - down 32%. Due to this move I have lost nearly USD 100,000 or 1/3 of my life savings - in just 9 months. I am sincerely puzzled how this could happen considering that gold is the "safe haven" asset. I can only surmise that the globalist bankers, the radical socialists, and their allies in the Muslim Brotherhood are conspiring to discredit you and your associates at Goldline. On the positive side I have avoided the massive hyperinflation that we have experienced over the last year. Since I invested in gold the CPI has risen from 231.6 to 231.8 a 1/10th of 1% increase. Thank you so much for your help.

Your friend - ROB"

Ok in case you were wondering - I am not a moron. I did not really put my life savings into gold. But considering Glenn has nearly 1MM monthly listeners getting a constant dose of paranoia and gold-bug drivel I will bet that someone did exactly what I suggested in the above letter. Again I am not a moron, I did not invest in gold, and there is no hyperinflation. For more on this last point see Paul Krugman's response to Eric Erickson on the price of milk and bread (see here).

Actually to put this into perspective the writer of the fictitious letter above lost 1/3 of his savings over the last 9 months by investing in gold. How far back would we have to go in order for the loss due to inflation to be equal to a loss of 1/3 of savings? If you go back to June of 1996 the CPI was at 152. Today the CPI is at 231. Meaning that over the last 17 years a dollar has lost 1/3 of its purchasing power due to inflation (152/231 = .66). That is assuming you earned 0 interest on your savings.

Thursday, July 04, 2013

A hypothetical question about a hypothetical question...

First let me say that I have no evidence that this actually occurred. But it is my understanding that the Egyptian military and US military are pretty friendly. I wonder if the Egyptian military higher ups ran the idea of deposing President Morsi past their US counterparts? Not for approval but to see what the response would be. Something along the lines of "say we were to depose the president. Not that we are actually thinking about doing it. But just as a hypothetical. What would the backlash be. How negatively would it affect our relationship?" I have no idea if this actually happened but if it did I would be very curious as to what the response was...if it happened..which I have no evidence that it did.

Just Wondering...

From Washington Post June 18, 2013

Egypt appoints member of terror group that once massacred tourists to run tourism region

"It was only 16 years ago, in 1997, that members of an Egyptian militant group called Gamaa Islamiya stormed the ancient Temple of Hatshepsut in Luxor, a tourism magnet, and massacred 62 tourists before killing themselves, part of their insurgent campaign against the government. This week, Egyptian President Mohamed Morsi swore in Adel Mohamed al-Khayat, a former leader of Gamaa Islamiya and now a member of its political arm, as the new governor of Luxor governorate."

I wonder how much this incident contributed to the Egyptian military's willingness to overthrow President Morsi. Considering the Egyptian military spent years battling Gamaa Islamiya (see here) one could imagine how this appointment would have been received in the military camp. To be fair, al-Khayat resigned within a week but his appointment to this - of all possible positions - demonstrated incredible insensitivity.

Egypt appoints member of terror group that once massacred tourists to run tourism region

"It was only 16 years ago, in 1997, that members of an Egyptian militant group called Gamaa Islamiya stormed the ancient Temple of Hatshepsut in Luxor, a tourism magnet, and massacred 62 tourists before killing themselves, part of their insurgent campaign against the government. This week, Egyptian President Mohamed Morsi swore in Adel Mohamed al-Khayat, a former leader of Gamaa Islamiya and now a member of its political arm, as the new governor of Luxor governorate."

I wonder how much this incident contributed to the Egyptian military's willingness to overthrow President Morsi. Considering the Egyptian military spent years battling Gamaa Islamiya (see here) one could imagine how this appointment would have been received in the military camp. To be fair, al-Khayat resigned within a week but his appointment to this - of all possible positions - demonstrated incredible insensitivity.

Some thoughts on the Egyptian coup

I start from the premise that it is never a good thing for a democratically elected government be overthrown in a military coup.

However which of these two events was today's coup more like

Websters defines a constitution as either

Using this definition of constitution is is easy to see what went wrong with the drafting of the Egyptian Constitution. The document was written by a drafting committee made up predominantly of Muslim Brotherhood. When the constitution was put to a popular vote it received 63% of the vote but only 30% of the eligible population voted - meaning that only 19% of the eligible population voted in favor of the document. So large portions of the population did not in fact agree to the rules of the game. Even so last November President Morsi changed some of the rules of the game by announcing that his decrees were above judicial review.

Having said that I wonder if not for the bad state of the economy would Morsi still be in power. I tend to think yes. It was a combination of lack of legitimacy and deteriorating economic performance with no apparent plan for how to improve the situation - which pushed him out.

However which of these two events was today's coup more like

- A lightening bolt hits your house.

- A couple decides to divorce after a bad three year marriage.

Websters defines a constitution as either

- an established law or custom: ordinance

- the mode in which a state or society is organized; especially: the manner in which sovereign power is distributed

- the basic principles and laws of a nation, state, or social group that determine the powers and duties and the government and guarantee certain rights to the people in it

- a written instrument embodying the rules of a political or social organization

However my friend Leonard Wantchekon would argue that a constitution is not just a set of rules by which country is to be governed. Rather it is a set of rules for power sharing by which parties agree to band together to form a coalition. The rules contained within the constitution must be attractive enough to get all parties to agree to enter into the coalition. Some of the rather strange aspects of the the original Constitution of the United States (the Senate, the 2/3 person rule) were concessions to woo small states and slave holding southern states into the coalition. The US Civil War occurred when one party to the coalition (the Southern states) decided they no longer wanted to abide by the rules of the constitution and struck out on their own. Lincoln later used the opportunity of the war to redefine the rules of the constitution.

Using this definition of constitution is is easy to see what went wrong with the drafting of the Egyptian Constitution. The document was written by a drafting committee made up predominantly of Muslim Brotherhood. When the constitution was put to a popular vote it received 63% of the vote but only 30% of the eligible population voted - meaning that only 19% of the eligible population voted in favor of the document. So large portions of the population did not in fact agree to the rules of the game. Even so last November President Morsi changed some of the rules of the game by announcing that his decrees were above judicial review.

So is this more like the lightening bolt or the divorce?

Having said that I wonder if not for the bad state of the economy would Morsi still be in power. I tend to think yes. It was a combination of lack of legitimacy and deteriorating economic performance with no apparent plan for how to improve the situation - which pushed him out.

Wednesday, July 03, 2013

A truly strange response to a bit of good fortune...

The Republican Party has been saying that it wants to reach out to minority voters. So here is a most fortuitous opportunity. A minority woman, who is a former Miss America and a Harvard law school graduate, and is also a conservative.. says that she wants to run as a Republican candidate for the US House of Representatives 13th District of Illinois. If I were the party chair from her district I would be jumping up and down celebrating. Ok maybe not quite celebrating...the seat is currently held by a Republican but it is a swing district and the Ds are targeting it for the next election. Still I would be trying to nurture this candidate perhaps not for this seat and this race but for the future. But I guess that is where Montgomery County GOP Chairman Jim Allen I differ. Here is his exact response...

"Rodney Davis will win and the love child of the D.N.C. will be back in S—cago by May of 2014 working for some law firm that needs to meet their quota for minority hires. The truth is Nancy Pelosi and the DEMOCRAT party want this seat. So they called RINO Timmy Johnson to be their pack mule and get little queen to run. Ann Callis gets a free ride through a primary and Rodney Davis has a battle. The little queen touts her abstinence and she won the crown because she got bullied in school,,,boohoo..kids are cruel, life sucks and you move on..Now, miss queen is being used like a street walker and her pimps are the DEMOCRAT PARTY and RINO REPUBLICANS…These pimps want something they can’t get,,, the seat held by a conservative REPUBLICAN Rodney Davis and Nancy Pelosi can’t stand it...Little Queenie and Nancy Pelosi have so much in common but the one thing that stands out the most.. both are FORMER QUEENS, their crowns are tarnished and time has run out on the both of them..”"

Apparently that strategy didn't work so well as Jim Allen has resigned as Montgomery County Chair. Well if they need someone who is a bit more strategically savvy...I am available. lllinois 13 is on the southwest side of the city of Chicago. Btw her name is Erika Harold

"Rodney Davis will win and the love child of the D.N.C. will be back in S—cago by May of 2014 working for some law firm that needs to meet their quota for minority hires. The truth is Nancy Pelosi and the DEMOCRAT party want this seat. So they called RINO Timmy Johnson to be their pack mule and get little queen to run. Ann Callis gets a free ride through a primary and Rodney Davis has a battle. The little queen touts her abstinence and she won the crown because she got bullied in school,,,boohoo..kids are cruel, life sucks and you move on..Now, miss queen is being used like a street walker and her pimps are the DEMOCRAT PARTY and RINO REPUBLICANS…These pimps want something they can’t get,,, the seat held by a conservative REPUBLICAN Rodney Davis and Nancy Pelosi can’t stand it...Little Queenie and Nancy Pelosi have so much in common but the one thing that stands out the most.. both are FORMER QUEENS, their crowns are tarnished and time has run out on the both of them..”"

Apparently that strategy didn't work so well as Jim Allen has resigned as Montgomery County Chair. Well if they need someone who is a bit more strategically savvy...I am available. lllinois 13 is on the southwest side of the city of Chicago. Btw her name is Erika Harold

Subscribe to:

Comments (Atom)